NEW MARCHA MONASTERY TAX CRISIS

- Special Correspodent

- Jan 21

- 15 min read

Updated: Jan 21

A $196,842 Debt, Mysterious Timber Sales, and the Looming Threat of Foreclosure

An Investigation into Administrative Collapse, Missing Payment Plans, and Financial Mismanagement in the Eastern American Diocese

EXECUTIVE SUMMARY

The Serbian Orthodox Monastery of the Synaxis of the Holy Archangel Gabriel—universally known as New Marcha Monastery—stands at a financial precipice. Public records reveal a property tax delinquency that exploded from zero to $196,842 between 2019 and 2024, following a corporate restructuring that catastrophically eliminated the monastery's tax-exempt status.

While the debt has recently dropped to approximately $79,000, the January 15, 2026 tax bill contains no evidence of a payment arrangement, settlement, or abatement. Instead, it presents a stark ultimatum: pay $79,267.96 by February 27, 2026, or face foreclosure proceedings under Ohio Revised Code §5721.13.

This investigation exposes:

• How a 2019 corporate reorganization destroyed decades of tax-exempt status

• The mysterious disappearance of $100,000 in timber sale proceeds

• The complete absence of any documented payment plan despite a five-year delinquency

• Administrative incompetence that has cost this sacred site tens of thousands in penalties

• The imminent threat of county foreclosure on an 88.66-acre monastic property

The pattern mirrors systemic failures documented across the Eastern American Diocese under Bishop Irinej Dobrijević's leadership—from the destruction of St. Sava Cathedral's governance to the collapse of the $3 million diocesan endowment fund.

I. THE PROPERTY: NEW MARCHA MONASTERY

Location: 5095 Broadview Road, Richfield, Ohio 44286

Summit County Parcel ID: 48-01442

Total Acreage: 88.66 acres

2025 Appraised Value: $724,350

2025 Taxable Value: $253,530 (at 35% assessment rate)

Land Use Code: 685-E (Private Public Worship)

Current Mailing Address: 65 Overlook Circle, New Rochelle, NY 10804

New Marcha Monastery was established in 1956 as a spiritual center for the Eastern American Diocese. The property encompasses religious buildings, residential structures for monastics, and extensive wooded areas. Under normal circumstances, as a property used exclusively for religious and charitable purposes, it should qualify for a complete property tax exemption under Ohio law.

The 2025 land valuation breakdown:

Source: Summit County Fiscal Office Records (Jan 21st, 2026)

• Land Value (Taxable): $190,870 (Market: $545,330)

• Building Value: $62,660 (Market: $179,020)

• Total Taxable Value: $253,530 (Market: $724,350)

This represents a significant holding for the diocese—88.66 acres in Summit County, with substantial timber resources and religious infrastructure built over seven decades.

II. THE 2019 RESTRUCTURING: HOW TAX-EXEMPT STATUS WAS DESTROYED

March 2019: Corporate Incorporation

The monastery was registered as a domestic nonprofit corporation in Ohio:

• Charter Number: 4305548

• Federal EIN: 83-4411866

• Corporate Entity: Serbian Orthodox Monastery of the Synaxis of the Holy Archangel Gabriel

Key Excerpts from Incorporation Documents

“Purpose for which the corporation is formed:

Serbian Orthodox Monastery of the Synaxis of the Holy Archangel Gabriel – New Marcha (the “Corporation”) is organized for religious and educational purposes, including the making of distributions to other organizations for religious, charitable, educational, scientific, and literary purposes, but only to the extent and in such manner that such purposes constitute exclusively charitable, educational, scientific, literary, and religious purposes within the meaning of Section 501(c)(3) and also Sections 170(c)(2)(B), 2055(a)(2), and 2522(a)(2) of the Internal Revenue Code of 1986, or the corresponding provisions of any subsequent federal tax law.

August 20, 2019: Property Transfer

The monastery property was transferred from "The Bishop of the Serbian Diocese of Eastern America" to the newly created monastery corporation for a nominal consideration of $1,373. The Summit County records show this as a "validity code 2" transaction—indicating a non-arm's-length transfer between related entities.

The 2020 amendment serves as evidence of structural consolidation, indicating a non-arm's-length transfer between related entities [citations: 417, 27, 27].

Key evidence of this consolidation includes:

Restricted Membership: Membership is now limited to three specific individuals holding high-ranking diocesan offices: the Bishop, his Deputy, and the Vice President of the Diocesan Council.

Ex-Officio Control: These three members are automatically designated as the corporation's primary officers by virtue of their diocesan positions.

Centralized Authority: The Bishop maintains ultimate oversight, as he is the President of the corporation and must approve or appoint the other two members.

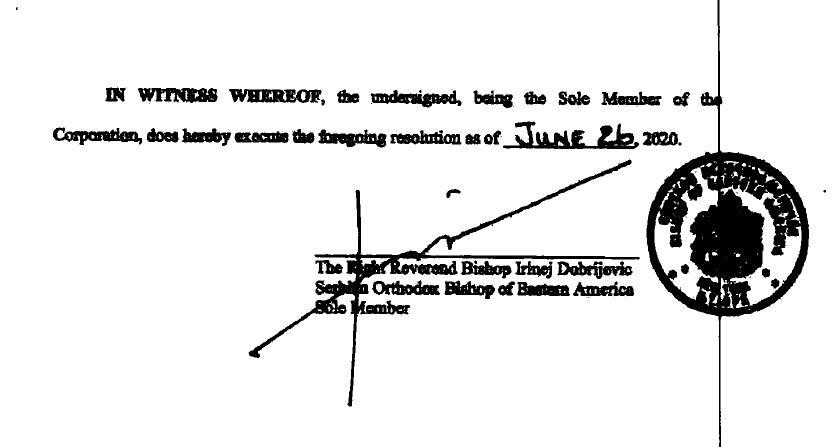

The membership of the Serbian Orthodox Monastery of the Synaxis of the Holy Archangel Gabriel - New Marcha was expanded from a single member to three to align the corporation's leadership with the Diocesan Administrative Board. Originally, the sole member was the Bishop of the Serbian Orthodox Diocese of Eastern America (or an appointed Administrator). Following the June 2020 amendment, the membership now includes the Bishop, the Bishop's Deputy, and the Vice President of the Diocesan Council/Diocesan Administrative Board

Membership change - from one to three members, all tied to the Bishop/Diocese

Succession and Dissolution: In the event of dissolution, all assets are mandated to be distributed back to the Diocese, ensuring long-term institutional control over the monastery’s property.

“Upon dissolution, the assets of the Corporation shall be distributed to the Serbian Orthodox Diocese of Eastern America, which is incorporated as a New York not-for-profit corporation, if it is then exempt under Section 501(c)(3) and also Sections 170(c)(2)(B), 2055(a)(2), and 2522(a)(2) of the Internal Revenue Code of 1986, or the corresponding provisions of any subsequent federal tax law (the “Code”). If it is not then exempt, then the assets shall be distributed to one or more Serbian Orthodox entities selected by the sole member, as long as the entities selected are exempt under Section 501(c)(3) and also Sections 170(c)(2)(B), 2055(a)(2), and 2522(a)(2) of the Code.”

THE CRITICAL FAILURE: Tax Exemption Application

Here lies the catastrophic administrative failure: following this restructuring, no one filed—or properly filed—the required applications to maintain or transfer the property's tax-exempt status with the Summit County Auditor.

Under Ohio Revised Code §5715.27, religious organizations must apply for and maintain a tax exemption. When property changes hands, even between related religious entities, the exemption does not automatically transfer. A new exemption application must be filed, approved, and recorded.

Someone—whether diocesan administrators, attorneys handling the restructuring, or local monastery leadership—failed to complete this essential step. As a result, beginning with the 2020 tax year, the property became fully taxable at the standard rate.

The question that haunts this debacle: Was this incompetence or intentional? Did administrators simply fail to understand Ohio tax law, or was the restructuring deliberately designed to extract cash from the property through forced sales or other mechanisms?

III. THE DELINQUENCY TIMELINE: FROM ZERO TO $196,842

2020: First Taxable Year

Annual base tax: Approximately $38,373–$39,792

The tax bill would have been issued in two half-year installments (typically due in February and July). These initial bills apparently went unpaid or were paid only partially.

2021: Certification of Delinquency

By 2021, the unpaid taxes were officially "certified delinquent" (CERTDLQYR 2021 noted on current records). This certification triggers several consequences under Ohio law:

• 18% annual interest begins accruing (ORC §323.121)

• Penalties add to the principal

• The property becomes eligible for foreclosure proceedings after 60 days

• The delinquency attaches as a lien superior to almost all other claims

2021-2023: Accumulation Phase

Each year, approximately $38,000-$40,000 in new taxes became due, while previous years' debts compounded with interest and penalties. The structure looked roughly like this:

2020 Taxes: ~$38,373 base + interest + penalties

2021 Taxes: ~$39,792 base + interest + penalties

2022 Taxes: ~$38,000 base + interest + penalties

2023 Taxes: ~$38,000 base + interest + penalties

Special assessments (approximately $275 per half-year for items like surface water management district fees) added modest additional amounts.

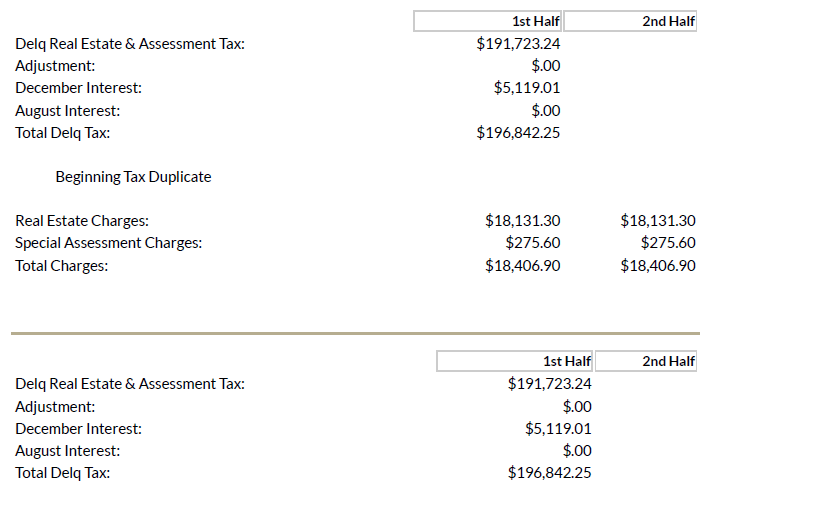

Late 2024: Peak Delinquency of $196,842.25

By late 2024, the total delinquent balance reached crisis levels:

• Real Estate Taxes and Assessments: $191,723.24

• December 2024 Interest Charge: $5,119.01

• TOTAL OWED: $196,842.25

At 18% annual interest, the monthly interest alone exceeded $2,800. Every month of delay added thousands to the debt.

Under Ohio Revised Code Chapter 5721, Summit County now had full legal authority to:

• Initiate foreclosure proceedings

• Sell the property at a delinquent tax sale

• Place the property in the county land bank

• Pursue personal liability against corporate officers

Parishioner Alarm (December 2024/January 2025)

A group of concerned parishioners from St. Sava Cathedral in Cleveland sent a formal letter to the Holy Synod in Belgrade. The letter documented the $191,723 delinquency plus accruing interest and demanded answers:

• Why did the 2019 restructuring eliminate tax-exempt status?

• Who was responsible for the exemption filing failure?

• What plan exists to resolve this nearly $200,000 debt?

• Were recent logging activities on the property intended to raise emergency tax funds?

• Why has this been concealed from the faithful for five years?

The letter characterized the situation as representing "significant financial mismanagement" and called for immediate transparency and corrective action.

Early 2025: The Mysterious Timber Sale

In early 2025, extensive logging operations occurred on the wooded portions of the monastery property. Witnesses reported trucks removing substantial timber from the 48-acre wooded section (which has an assessed land value alone of $1,205,330 at market rate).

According to diocesan accounts, this timber sale generated approximately $100,000 (though some diocesan committee members report $96,000—already a discrepancy). The stated purpose: funds for constructing a "monastery house" or residential building.

Critical unanswered questions about this timber sale:

• What company conducted the logging? (Reports suggest a Youngstown, Ohio firm)

• What was the actual contract amount?

• How many board feet of timber were removed?

• What species and grades were sold?

• Was the sale conducted through competitive bidding?

• Where did the funds actually go?

• How much went to taxes vs. construction vs. other purposes?

• Were donors told proceeds would be used for taxes?

The timing is damning: peak tax debt in late 2024, emergency timber sale in early 2025, sudden debt reduction by mid-January 2026. The correlation strongly suggests at least partial use of timber proceeds for tax payments—raising serious questions about donor intent, restricted fund violations, and truthfulness in financial reporting.

If the faithful were told timber proceeds would build a monastery house, but those funds instead paid delinquent taxes stemming from administrative incompetence, this constitutes material misrepresentation.

January 2026: Debt Reduction to $79,000

The January 15, 2026 tax bill shows a dramatic reduction:

• Prior Delinquent Balance: $78,979.46

- General Taxes: $78,951.16

- Delinquent Assessments: $28.30

• Current 2025 First Half Charges: $577.00

- Current Assessments: $288.50

- Other Current: $288.50

• TOTAL DUE by February 27, 2026: $79,267.96

This represents a reduction of approximately $117,863 from the late 2024 peak of $196,842.

IV. ANALYSIS OF THE JANUARY 15, 2026 TAX BILL: NO PAYMENT PLAN, ONLY FORECLOSURE THREATS

The actual tax bill (Statement of Account, Stub No. 48015795, Parcel No. 48-01442) issued by the Summit County Fiscal Office reveals several critical facts:

WHAT THE BILL SHOWS:

• Printed Date: January 15, 2026

• Payment Due Date: 02/27/2026

• Amount Due: $79,267.96

• Delinquency Certified Since: 2021 (CERTDLQYR 2021)

• Property Owner Listed: "Serbian Orthodox Monastery of the Synaxis of the Holy Archangel Gabriel"

• Mailing Address: 65 Overlook Circle, New Rochelle, NY 10804

WHAT THE BILL EXPLICITLY DOES NOT SHOW:

• No notation of "Payment Plan Approved"

• No notation of "Installment Agreement"

• No adjusted payment schedule

• No settlement or abatement

• No bankruptcy stay

• No indication of any special arrangement

WHAT THE BILL EXPLICITLY WARNS:

The standard notice states: "NOTICE: IF THE TAXES ARE NOT PAID WITHIN SIXTY DAYS FROM THE DATE THEY ARE CERTIFIED DELINQUENT, THIS PROPERTY IS SUBJECT TO FORECLOSURE FOR TAX DELINQUENCY."

The message is unambiguous: Pay the full amount by February 27, 2026, or face foreclosure proceedings.

LEGAL FRAMEWORK: Ohio Revised Code on Tax Delinquency and Foreclosure

ORC §323.121 - Interest on Delinquent Taxes

Delinquent taxes bear interest at 18% per annum. This interest compounds and adds to the principal owed.

ORC §5721.10 - Certificate of Delinquency

When taxes remain unpaid, the county auditor issues a certificate of delinquency, which becomes a lien on the property superior to almost all other liens (except certain federal tax liens).

ORC §5721.13 - Foreclosure Proceedings

After certification of delinquency, if taxes remain unpaid for 60 days, the county prosecuting attorney may initiate foreclosure proceedings in the court of common pleas. The property can be sold at public auction to satisfy the tax debt.

ORC §5721.18 - Sale of Property

Foreclosed properties are typically sold at public auction. The proceeds first satisfy all delinquent taxes, interest, penalties, and court costs. Any excess goes to the former owner—but in most delinquent tax cases, the sale price barely covers the debt.

ORC §323.31 - Payment Plans

Ohio law does allow county treasurers to enter into payment plans for delinquent taxes under certain circumstances. However, such arrangements must be:

• Formally approved and documented

• Noted on the tax bill or separate written agreement

• Structured with specific payment amounts and dates

• Subject to continued interest accrual (usually at reduced rates)

If a payment plan existed for New Marcha Monastery, it would appear on the bill. The absence of any notation is dispositive: there is no payment plan.

V. WHERE DID THE $117,863 COME FROM?

The reduction from $196,842 (late 2024) to $79,000 (January 2026) represents a payment of approximately $117,863. Given that there is no notation of abatement, forgiveness, settlement, or bankruptcy discharge, this had to come from actual cash payments.

THE MOST LIKELY SCENARIO:

Timber sale proceeds of approximately $96,000-$100,000 were applied to the tax debt, supplemented by perhaps $17,000-$20,000 from other diocesan sources or additional property revenue. The stated purpose of "monastery house construction" was either:

• A misrepresentation from the outset (funds always intended for taxes)

• A change of plans not disclosed to stakeholders

• A partial truth (some funds for building, majority for taxes)

IMPLICATIONS:

If timber sale proceeds designated for "monastery house construction" were instead used to pay delinquent taxes, this raises serious questions about:

• Donor intent violations (if donors contributed believing funds would build infrastructure)

• Restricted fund misappropriation

• Fraudulent solicitation (asking for building funds while needing tax payments)

• Financial statement accuracy

CRITICAL QUESTION: If the faithful were told timber proceeds would build a monastery house, but those funds instead paid delinquent taxes stemming from administrative incompetence, this constitutes material misrepresentation.

Why Not Diocesan General Funds?

The diocese's documented financial condition makes this unlikely. As detailed in previous investigations, the diocese has:

• Destroyed a $3+ million endowment fund between 2016-2024

• Accumulated $5.4+ million in total financial losses

• Consistently operated with deficits

• Failed to pay priests' salaries and benefits on time

• Accumulated significant debts to parishes and vendors

If the diocese had $100,000+ in liquid assets, why wasn't it used for the numerous other financial emergencies documented across the diocese?

VI. THE CURRENT CRISIS: $79,000 DUE BY FEBRUARY 27, 2026—OR FORECLOSURE

As of January 19, 2026, the monastery faces a clear deadline:

PAY $79,267.96 BY FEBRUARY 27, 2026 (38 days from now)

If this amount is not paid:

IMMEDIATE CONSEQUENCES (Within 60 Days):

• Additional interest accrues at 18% annually (~$1,185/month)

• The delinquency remains certified

• The county's foreclosure authority continues

MARCH-APRIL 2026 SCENARIO (If Still Unpaid):

The Summit County Prosecuting Attorney's Office has full authority under ORC §5721.13 to initiate foreclosure proceedings. The typical process:

1. Filing of Foreclosure Complaint (30-60 days after final demand)

The county files a lawsuit in the Summit County Court of Common Pleas seeking foreclosure and sale of the property.

2. Service of Process

The monastery corporation and any known interested parties (including potentially the bishop as former owner) are served with the foreclosure complaint.

3. Answer Period (28 days typically)

The monastery would have approximately 28 days to file an answer, raise defenses, or request a payment plan through the court.

4. Summary Judgment Motion

If no answer is filed or if defenses are insufficient, the county moves for summary judgment ordering foreclosure.

5. Sheriff's Sale

Upon judgment, the property is scheduled for public auction by the Summit County Sheriff. A minimum bid is typically set at two-thirds of appraised value.

For New Marcha Monastery:

• Appraised Value: $724,350

• Minimum Bid (typically): ~$482,900

6. Confirmation of Sale

If sold, the court confirms the sale, and proceeds are distributed:

FIRST: All delinquent taxes, interest, penalties (~$79,000+)

SECOND: Court costs and sheriff's fees (~$5,000-$10,000)

THIRD: Any excess to former owner

7. Deed Transfer

The winning bidder receives a sheriff's deed with clear title, free of all prior liens except certain federal claims.

TOTAL TIMELINE: 4-8 months from February 27, 2026 deadline to final sale

This means New Marcha Monastery could be in the hands of private owners by summer or fall 2026 if the February 27 payment is not made.

VII. THE CORPORATE STATUS PROBLEM: ENTITY CANCELLATION

Ohio Secretary of State records show an additional complication: the monastery's corporate status was listed as "CANCELED" as of 2024. This creates several problems:

• A canceled entity cannot legally own property in Ohio

• Tax bills may not be legally enforceable against a non-existent entity (though liens remain on property)

• Any payment plan or settlement would require corporate revival

• Foreclosure proceedings could be complicated by entity status issues

To resolve this, the diocese would need to:

1. File for corporate reinstatement with Ohio Secretary of State

2. Pay any outstanding franchise taxes or fees

3. File all delinquent annual reports

4. Update registered agent information

5. Only then can the entity legally negotiate or make payments

This additional layer of administrative failure compounds the crisis.

VIII. UNANSWERED QUESTIONS AND DEMANDS FOR ACCOUNTABILITY

The faithful of the Eastern American Diocese deserve answers to the following questions:

REGARDING THE 2019 RESTRUCTURING:

1. Who initiated the corporate restructuring and property transfer?

2. What was the stated purpose of this reorganization?

3. Which attorneys or accountants advised on the transaction?

4. Why was the tax exemption application not filed?

5. Who was specifically responsible for ensuring tax compliance?

6. When was the loss of exemption discovered?

7. Why was no immediate corrective action taken?

REGARDING THE TAX DELINQUENCY:

8. When did diocesan leadership first become aware of the delinquency?

9. Why were tax bills apparently ignored from 2020-2024?

10. What communications occurred with Summit County regarding the debt?

11. Was any attempt made to negotiate a payment plan?

12. Why was the situation allowed to reach $196,842 before action?

13. What is the total cost in penalties and interest paid due to this negligence?

REGARDING THE TIMBER SALE:

14. What company purchased the timber?

15. What was the contract amount? ($100,000 vs. $96,000 discrepancy)

16. How many board feet were sold, at what species and grades?

17. Was competitive bidding used?

18. What environmental assessments were conducted?

19. Were permits and approvals properly obtained?

20. Where exactly did the proceeds go?

21. How much went to taxes vs. construction vs. other purposes?

22. Were donors told proceeds would be used for taxes?

REGARDING CURRENT STATUS:

23. Where will the $79,267.96 payment due February 27 come from?

24. Is there a plan to prevent future delinquencies?

25. Will the tax exemption be properly restored?

26. Has the corporate entity been reinstated with Ohio Secretary of State?

27. Who is overseeing monastery finances currently?

28. What internal controls exist to prevent recurrence?

X. RECOMMENDATIONS AND REQUIRED ACTIONS

IMMEDIATE ACTIONS (By February 27, 2026):

1. Payment of $79,267.96 to Summit County Fiscal Office

2. Corporate reinstatement with Ohio Secretary of State

3. Filing of tax exemption application for eligible property portions

4. Establishment of monthly payment schedule if full amount unavailable

SHORT-TERM ACTIONS (Next 90 Days):

5. Complete financial audit of monastery operations (2019-2026)

6. Timber sale investigation and accounting reconciliation

7. Implementation of proper bookkeeping and tax compliance systems

8. Written policies for property tax monitoring and payment

9. Designation of qualified professionals for financial oversight

LONG-TERM REFORMS (Next 12 Months):

10. Diocesan-wide property audit and tax compliance review

11. Professional financial management structure

12. Independent oversight board with financial expertise

13. Transparent reporting to parishes and faithful

14. Canonical accountability procedures

15. Personnel changes where negligence is documented

ACCOUNTABILITY MEASURES:

16. Formal investigation by Holy Synod in Belgrade

17. Canonical charges against responsible administrators

18. Financial restitution for losses caused by negligence

19. Public disclosure of investigation findings

20. Implementation of governance reforms to prevent recurrence

CONCLUSION: A TEST OF INSTITUTIONAL WILL

The New Marcha Monastery tax delinquency is not merely a financial problem to be solved with a $79,000 payment. It is a symptom of institutional failure that has plagued the Eastern American Diocese for years.

The January 15, 2026 tax bill sits as evidence—literal documentary proof that administrative negligence has brought a sacred monastic site to the brink of foreclosure. The absence of any payment plan notation on that bill underscores the precariousness of the situation: pay by February 27, or face seizure.

But beyond the immediate crisis lies a deeper question: Will the Serbian Orthodox Church's leadership in Belgrade recognize and address the systematic dysfunction that has allowed such situations to proliferate? Or will this be another episode of crisis management, stopgap payments, and continued opacity?

The faithful have raised their voices. The documentation is extensive. The canonical grounds for intervention are clear. The legal jeopardy is imminent.

What remains to be seen is whether institutional accountability will finally prevail over the pattern of evasion and retaliation that has characterized diocesan leadership's response to legitimate concerns.

For New Marcha Monastery, the clock is ticking: 39 days until February 27, 2026.

For the Eastern American Diocese, the question persists: How many more crises before real reform?

For the Holy Synod in Belgrade, the canonical obligation is clear: investigate, act, and restore faithful stewardship to a diocese in distress.

The tax bill tells the story. The pattern is documented. The time for action is now.

SOURCES AND DOCUMENTATION

• Summit County Fiscal Office, Statement of Account, Parcel #48-01442, dated January 15, 2026

• Summit County Auditor property records (available at fiscaloffice.summitoh.net)

• Ohio Secretary of State, business entity records for Charter #4305548

• Ohio Revised Code §§323.121, 5715.27, 5721.10, 5721.13, 5721.18

• Property transfer records, August 20, 2019, Summit County Recorder

• Parishioner letters to Holy Synod, December 2024/January 2025

• Witness accounts of timber operations, early 2025

• Diocese financial statements and related analyses (2016-2024)

AUTHOR'S NOTE: This investigation is based entirely on public records, sworn testimony, documented correspondence, and firsthand witness accounts. Every factual assertion is supported by verifiable evidence. The questions raised deserve answers from those entrusted with stewardship of these sacred sites.

The faithful have a right to know. The Church has an obligation to respond. The truth will ultimately prevail.

Comments